Opening Ceremony lays the foundation for cross-sector collaboration and breakthrough solutions.

10-14 JANUARY 2027 Abu Dhabi, UAE

EN

The Zayed Sustainability Prize Awards Ceremony celebrates 11 winners driving real-world impact across the categories of Health, Food, Energy, Water, Climate Action and Global High Schools.

The ADSW Summit sparks dynamic, inclusive discussions that drive the global sustainability agenda forward.

This Global South–focused gathering will convene policymakers, developers, financiers, and off-takers from the Global South and the UAE.

Blue Forum will focus on mobilizing $100 billion in water and ocean investment by 2030.

Read the latest thoughts and analysis on breakthrough solutions driving impact for a sustainable future

Explore reports and strategic insights from ADSW

Line of Sight Podcast brought to you by ADSW

Hear influential voices discuss global challenges and the solutions for a sustainable future

Subscribe to get the latest news, events and announcements

Open to all, the competition will accept submissions until November 16, 2025.

Get insights from crucial conversations throughout the global sustainability calendar

Watch virtual conversations with thought leaders and experts around the world

Find out why we convene the global sustainability community each year

See the sustainability experts helping guide ADSW's strategy

Read our story

Be part of a leading global sustainability platform

See the leaders from across sectors and around the world who have joined ADSW

A global leader in sustainability, Masdar has hosted ADSW since 2008

The Resilience Imperative: energy, supply chains, and the compounding cost of fragility

19 JUNE 2026

1678

Alicia Eastman, Managing Director, APC Investors, Co-Founder & Board Member, InterContinental Energy

The shocks have not arrived in isolation, leaving no time to address each ripple effect. COVID-19 fractured global supply chains just as geopolitical fault lines began to widen. The Russian invasion of Ukraine then removed one of the world's largest energy exporters from stable commerce almost overnight, sending natural gas prices in Europe to levels that would have seemed fantastical two years prior. Now, renewed conflict in the Arabian Gulf threatens maritime corridors through which a significant share of the world's seaborne oil transits daily. And layered across all of this is a new era of aggressive tariff regimes that have introduced structural uncertainty into the very trade relationships energy infrastructure depends upon.

The cumulative effect goes beyond economic disruption to a fundamental re-exposure of a vulnerability that decades of globalization had allowed us to obscure: energy systems built for efficiency and not resilience cannot hold when the world stops cooperating.

The chain reaction not priced in

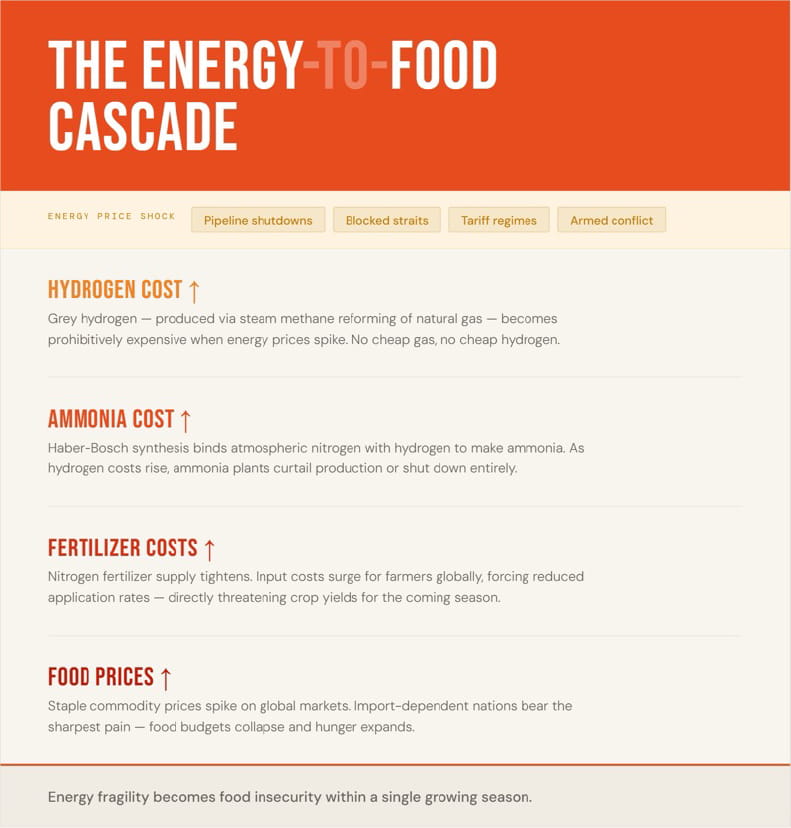

Energy is not one input among many, it is the input beneath all inputs. When energy prices spike, whether from a pipeline shutdown, a blocked strait, or a punitive import tariff, the consequences cascade through every sector that moves, heats, cools, manufactures, or grows anything.

The fertilizer chain illustrates this with uncomfortable clarity. The majority of the world's nitrogen fertilizers are produced via the Haber-Bosch process, which synthesizes ammonia from hydrogen that is derived almost entirely from natural gas. When European gas prices quadrupled in the wake of the Ukraine invasion, ammonia plants shuttered across the continent. Higher fertilizer prices translated directly into higher food production costs globally, with the sharpest pain felt in import-dependent nations across Africa, the Middle East, and South Asia. Energy fragility had become food insecurity within a single growing season.

Transport compounds the problem. Nearly every manufactured good, from semiconductors to steel, requires energy-intensive logistics. When fuel costs are volatile, freight costs become unpredictable, and businesses absorb or pass on costs that distort investment decisions across entire industries. The tariff environment of 2025–2026 has added a second layer of unpredictability to the same supply chains already stressed by energy volatility, creating a compounding effect that makes long-term capital planning genuinely difficult.

Redefining resilience in practice

Resilience in energy systems means something specific: the ability to maintain affordable, reliable access to energy across a range of adverse scenarios. This is the energy trilemma, balancing security, sustainability, and affordability. The shocks of the past five years have demonstrated that optimizing for any one dimension at the expense of the others creates dangerous brittleness.

Nations that had grown heavily dependent on single suppliers, Germany on Russian pipeline gas being the paradigmatic case, discovered that low cost and high reliability are not the same thing. Diversification across energy partners, energy types, and delivery infrastructure is now understood as a baseline requirement for any serious national energy strategy.

The role of green electrons and molecules in this re-architecting is practical, not merely aspirational. Wind and solar, once they are built, are structurally immune to the geopolitical and commodity price risks that make fossil fuel systems fragile. A solar installation in southern Europe or the American Southwest does not become more expensive because of decisions made in Riyadh or Moscow. Domestically generated renewable electricity also creates the conditions for green hydrogen production, a pathway that, as costs continue to fall, will ultimately decouple ammonia and fertilizer production from natural gas entirely, severing one of the most consequential links in the energy-to-food vulnerability chain.

What implementation actually requires

The forward priority is not to choose between energy sources but to build systems that are deliberately redundant across them. For policymakers, this means accelerating interconnection infrastructure, including transmission lines, LNG import terminals, and green hydrogen/ammonia corridors, so that no single point of failure becomes a national crisis. For businesses, it means treating energy procurement strategy with the same analytical rigor applied to financial risk management: scenario-testing supply chains against price volatility, diversifying contracts, and investing in on-site generation or offshore imports from reliable partners where and when feasible.

For investors, the implication is clear: the transition to resilient energy systems represents one of the largest sustained capital deployment opportunities of the coming decade. The projects that combine reliability, decarbonization, and reduced geopolitical exposure will attract premium valuation because they are solving for what markets have demonstrably, repeatedly, and expensively failed to price: systemic risk.

The compounding shocks of recent years were not unforeseeable. They were, in many cases, foreseen and then deprioritized. The work now is to build systems in energy, food, and trade, where resilience is engineered in, not retrofitted after the next crisis has already arrived.